{kind=link}

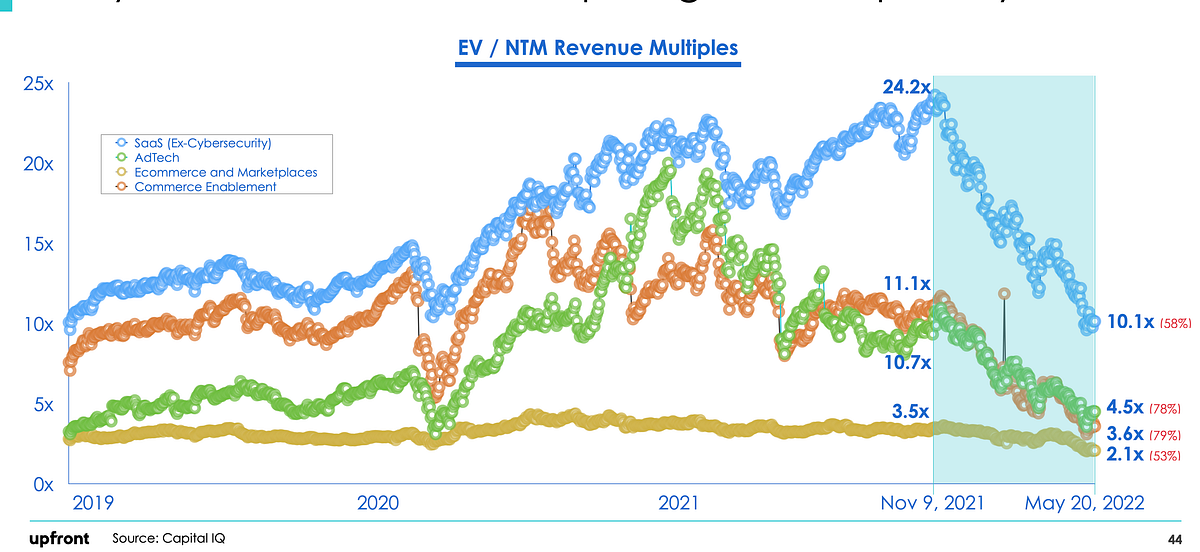

At our mid-year offsite our partnership at Upfront Ventures was discussing what the way forward for enterprise capital and the startup ecosystem regarded like. From 2019 to Might 2022, the market was down significantly with public valuations down 53–79% throughout the 4 sectors we have been reviewing (it’s since down even additional).

==> Apart, we even have a NEW LA-based associate I’m thrilled to announce: Nick Kim. Please observe him & welcome him to Upfront!! <==

Our conclusion was that this isn’t a brief blip that may swiftly trend-back up in a V-shaped restoration of valuations however moderately represented a brand new regular on how the market will worth these firms considerably completely. We drew this conclusion after a gathering we had with Morgan Stanley the place they confirmed us historic 15 & 20 12 months valuation developments and all of us mentioned what we thought this meant.

Ought to SaaS firms commerce at a 24x Enterprise Worth (EV) to Subsequent Twelve Month (NTM) Income a number of as they did in November 2021? Most likely not and we expect 10x (Might 2022) appears extra according to the historic pattern (really 10x remains to be excessive).

It doesn’t actually take a genius to appreciate that what occurs within the public markets is extremely more likely to filter again to the personal markets as a result of the last word exit of those firms is both an IPO or an acquisition (typically by a public firm whose valuation is mounted every day by the market).

This occurs slowly as a result of whereas public markets commerce every day and costs then alter immediately, personal markets don’t get reset till follow-on financing rounds occur which may take 6–24 months. Even then personal market traders can paper over valuation modifications by investing on the similar worth however with extra construction so it’s exhausting to grasp the “headline valuation.”

However we’re assured that valuations will get reset. First in late-stage tech firms after which it should filter again to Progress after which A and in the end Seed Rounds.

And reset they need to. Once you have a look at how a lot median valuations have been pushed up previously 5 years alone it’s bananas. Median valuations for early-stage firms tripled from round $20m pre-money valuations to $60m with loads of offers being costs above $100m. If you happen to’re exiting into 24x EV/NTM valuation multiples you may overpay for an early-stage spherical, maybe on the “higher idiot concept” however should you consider that exit multiples have reached a brand new regular, it’s clear to me: YOU. SIMPLY. CAN’T. OVERPAY.

It’s simply math.

No weblog publish about how Tiger is crushing all people as a result of it’s deploying all its capital in 1-year whereas “suckers” are investing over 3-years can change this actuality. It’s simple to make IRRs work very well in a 12-year bull market however VCs must become profitable in good markets and unhealthy.

Up to now 5 years among the greatest traders within the nation might merely anoint winners by giving them giant quantities of capital at excessive costs after which the media hype machine would create consciousness, expertise would race to hitch the following perceived $10bn winner and if the music by no means stops then all people is completely satisfied.

Besides the music stopped.

There’s a LOT of cash nonetheless sitting on the sidelines ready to be deployed. And it WILL be deployed, that’s what traders do.

Pitchbook estimates that there’s about $290 billion of VC “overhang” (cash ready to be deployed into tech startups) within the US alone and that’s up greater than 4x in simply the previous decade. However I consider it will likely be patiently deployed, ready for a cohort of founders who aren’t artificially clinging to 2021 valuation metrics.

I talked to a few buddies of mine who’re late-stage development traders they usually mainly instructed me, “we’re simply not taking any conferences with firms who raised their final development spherical in 2021 as a result of we all know there may be nonetheless a mismatch of expectations. We’ll simply wait till firms that final raised in 2019 or 2020 come to market.”

I do already see a return of normalcy on the period of time traders must conduct due diligence and ensure there may be not solely a compelling enterprise case but in addition good chemistry between the founders and traders.

I can’t communicate for each VC, clearly. However the way in which we see it’s that in enterprise proper now you’ve got 2 selections — tremendous dimension or tremendous focus.

At Upfront we consider clearly in “tremendous focus.” We don’t need to compete for the biggest AUM (belongings beneath administration) with the largest companies in a race to construct the “Goldman Sachs of VC” however it’s clear that this technique has had success for some. Throughout greater than 10 years we’ve stored the median first verify dimension of our Seed investments between $2–3.5 million, our Seed Funds principally between $200–300 million and have delivered median ownerships of ~20% from the primary verify we write right into a startup.

I’ve instructed this to folks for years and a few folks can’t perceive how we’ve been in a position to preserve this technique going by means of this bull market cycle and I inform folks — self-discipline & focus. After all our execution in opposition to the technique has needed to change however the technique has remained fixed.

In 2009 we might take a very long time to evaluate a deal. We might speak with prospects, meet your entire administration workforce, evaluate monetary plans, evaluate buyer buying cohorts, consider the competitors, and many others.

By 2021 we needed to write a $3.5m first verify on common to get 20% possession and we had a lot much less time to do an analysis. We frequently knew in regards to the groups earlier than they really arrange the corporate or left their employer. It compelled excessive self-discipline to “keep in our swimming lanes” of information and never simply write checks into the newest pattern. So we largely sat out fundings of NFTs or different areas the place we didn’t really feel like we have been the knowledgeable or the place the valuation metrics weren’t according to our funding targets.

We consider that traders in any market want “edge” … understanding one thing (thesis) or any individual (entry) higher than virtually some other investor. So we stayed near our funding themes of: healthcare, fintech, laptop imaginative and prescient, advertising and marketing applied sciences, online game infrastructure, sustainability and utilized biology and we’ve companions that lead every observe space.

We additionally focus closely on geographies. I feel most individuals know we’re HQ’d in LA (Santa Monica to be precise) however we make investments nationally and internationally. Now we have a workforce of seven in San Francisco (a counter wager on our perception that the Bay Space is an incredible place.) Roughly 40% of our offers are carried out in Los Angeles however practically all of our offers leverage the LA networks we’ve constructed for 25 years. We do offers in NYC, Paris, Seattle, Austin, San Francisco, London — however we provide the ++ of additionally having entry in LA.

To that finish I’m actually excited to share that Nick Kim has joined Upfront as a Companion based mostly out of our LA places of work. Whereas Nick can have a nationwide remit (he lived in NYC for ~10 years) he’s initially going to give attention to rising our hometown protection. Nick is an alum of UC Berkeley and Wharton, labored at Warby Parker after which most not too long ago on the venerable LA-based Seed Fund, Crosscut.

Anyone who has studied the VC business is aware of that it really works by “energy legislation” returns through which just a few key offers return the vast majority of a fund. For Upfront Ventures, throughout > 25 years of investing in any given fund 5–8 investments will return greater than 80% of all distributions and it’s typically out of 30–40 investments. So it’s about 20%.

However I assumed a greater mind-set about how we handle our portfolios is to consider it as a funnel. If we do 36–40 offers in a Seed Fund, someplace between 25–40% would seemingly see massive up-rounds inside the first 12–24 months. This interprets to about 12–15 investments.

Of those firms that grow to be nicely financed we solely want 15–25% of THOSE to pan out to return 2–3x the fund. However that is all pushed on the belief that we didn’t write a $20 million try of the gate, that we didn’t pay a $100 million pre-money valuation and that we took a significant possession stake by making a really early wager on founders after which partnering with them typically for a decade or extra.

However right here’s the magic few folks ever speak about …

We’ve created greater than $1.5 billion in worth to Upfront from simply 6 offers that WERE NOT instantly up and to the suitable.

The great thing about these companies that weren’t speedy momentum is that they didn’t elevate as a lot capital (so neither we nor the founders needed to take the additional dilution), they took the time to develop true IP that’s exhausting to duplicate, they typically solely attracted 1 or 2 sturdy rivals and we could ship extra worth from this cohort than even our up-and-to-the-right firms. And since we’re nonetheless an proprietor in 5 out of those 6 companies we expect the upside might be a lot higher if we’re affected person.

And we’re affected person.