{kind=link}

For a lot of Individuals, the significance of planning for retirement has lately turn out to be a necessary monetary precedence as many soon-to-be retirees are gearing as much as exit the workforce within the coming years.

As folks grow old, retirement planning takes a superior place amongst different monetary priorities. In a time the place the price of dwelling is consistently rising, towards the backdrop of an unsure future, planning in your monetary future turns into more and more difficult as you begin to age.

The state of retirement in America

In recent times, a number of research and surveys have discovered that it is turn out to be more and more onerous for Individuals to save lots of and enhance their retirement financial savings resulting from ongoing financial dangers

In a GOBankingRates survey of 1,000 Individuals aged 18 years and older, round 32.9% had not more than $100 of their financial savings account. An identical examine printed in 2022 discovered that just about 22% of Individuals had lower than $100 of their financial savings accounts.

There is no appropriate time or age to start out planning or saving for the long run, particularly when every thing appears to have so many added dangers lately.

In response to a Northwestern Mutual 2021 Planning & Progress Research, Individuals have lately been growing their retirement financial savings, with the common retirement financial savings account rising by 13% from $87,500 to $98,800.

Regardless of many bumping up their saving efforts, soon-to-be retirees, these aged 55 to 64 have a median financial savings stability of $120,000, whereas youthful U.S. adults, underneath 35 at present have a median account stability of $12,300 in line with a PwC report.

A lot of unplanned situations all through the previous few years have compelled many individuals into early retirement. Those that had been unable to correctly save and plan, have lately stepped out of retirement and again into the workforce as a method to financially maintain themselves.

The common age of retirement has elevated from 60 in 1990 to 66 in 2021 and with nearly all of adults now dwelling longer than beforehand, having fun with life after work could be pricey in the event you do not begin planning properly earlier than the age of retirement arrives.

Retirement calculation – chopping prices earlier than retirement

Financial uncertainty and rising prices have beckoned American adults to start out saving early on of their careers.

From this, analysis exhibits that for youthful earners, these born between 1981 and 1985, the retirement outlook is extra optimistic, as specialists predict them to have the best inflation-adjusted median annual revenue by the point they attain 70.

Early millennials, as they’re referred to as, will see a 22% enhance of their annual earnings as soon as they enter retirement, in comparison with pre-boomers, or these employees born between 1941 and 1945.

Technology Z, people aged 19 to 25 are even higher at saving for his or her future, with a majority of them placing away on common 14% of their revenue in line with one BlackRock examine printed final yr.

Youthful generations have extra confidence, and extra optimism in the case of planning for his or her retirement and future. Now with a majority of them taking on area within the workforce, monetary priorities will quickly start to vary, as many look to construct a nest egg that would final them by retirement.

Following a strict price range, chopping pointless bills, and studying learn how to work with cash are among the few issues many individuals are doing to cut back prices to stuff their retirement financial savings.

Scale back high-interest debt

Inflationary stress all through a lot of final yr has seen an more and more excessive variety of American adults lean on bank cards and private loans to assist them pay for on a regular basis bills. As of 2023, near half – 46% – of U.S. adults carry month-to-month debt, whether or not it is bank cards or different interest-related debt.

Preserving bills to a minimal can begin by lowering high-interest debt reminiscent of bank cards or private loans. For almost all of the working class, whereas it is nonetheless potential to afford it, it is advised to attenuate any curiosity debt you should still have, whilst you’re nonetheless receiving a month-to-month revenue.

Having this monetary security web means you are able to decrease your future bills and direct more money in the direction of extra essential monetary targets reminiscent of saving for retirement.

Taking management of your debt generally is a problem, as these bills are likely to accumulate over time, so it is best suggested to take a look at which funds could be handled at first, and whether or not it is potential to shorten the cost interval in order that it does not stretch into your retirement years.

Assess your insurance coverage protection

One other method to minimize bills early on in your profession is to evaluate your insurance coverage protection. As you turn out to be older, medical health insurance protection turns into an more and more essential product that you will want to hold for a lot of your golden years.

Taking the mandatory steps now to make sure you have the precise insurance coverage protection will show you how to higher perceive what sort of product it is best to take out, and what you’re paying for.

Typically folks solely take out insurance coverage protection later of their life, as soon as they’re in a snug monetary place. Whereas this is able to make sense on the time, insurance coverage merchandise are likely to turn out to be costlier as you age.

Whereas the distinction in merchandise could also be a number of {dollars} every month, over the long run these shortly add up. Talking to a monetary skilled or dealer will provide you with higher steering on which insurance coverage merchandise are finest for somebody in your place, and will provide you with probably the most advantages when you step into retirement.

Take management of scholar loans

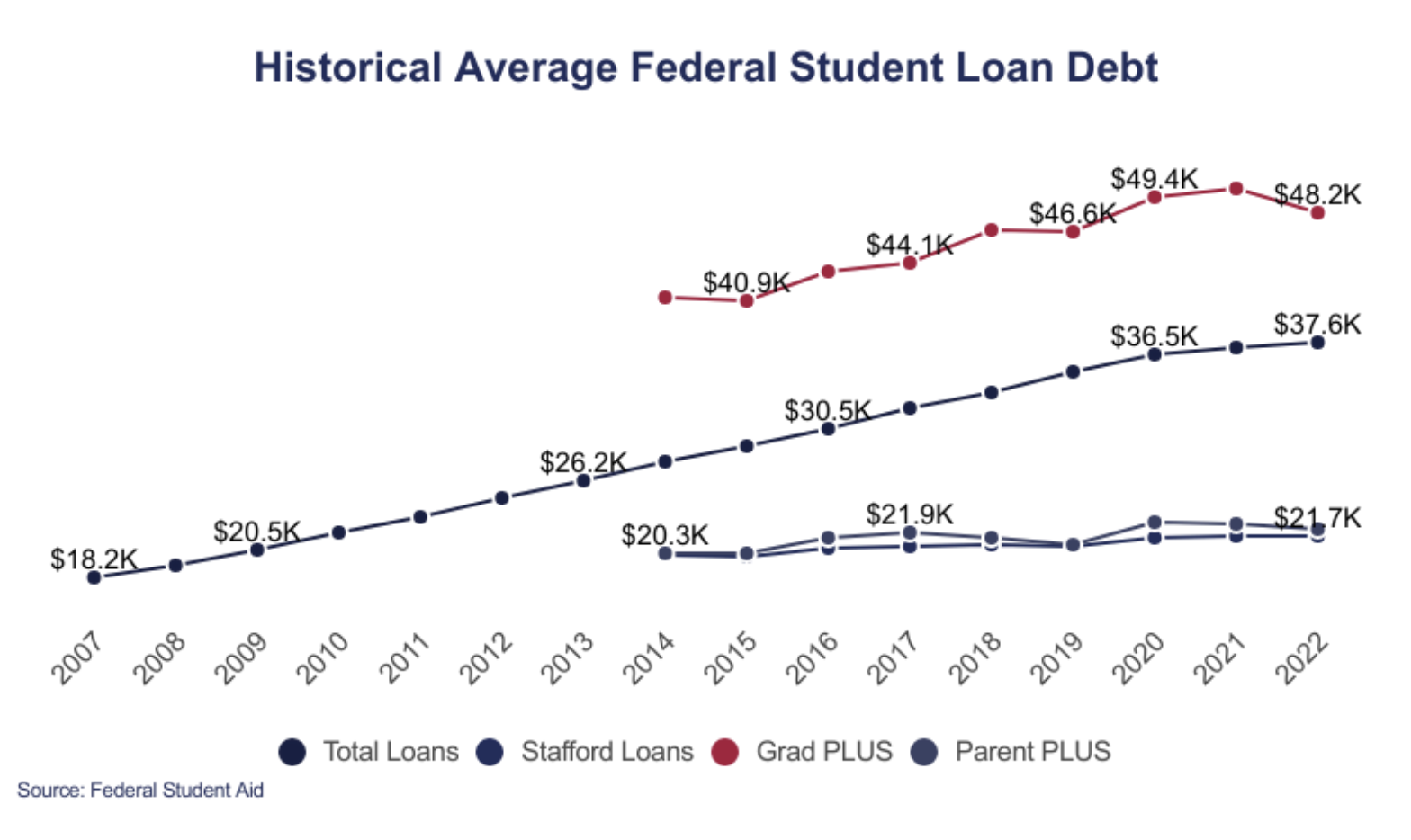

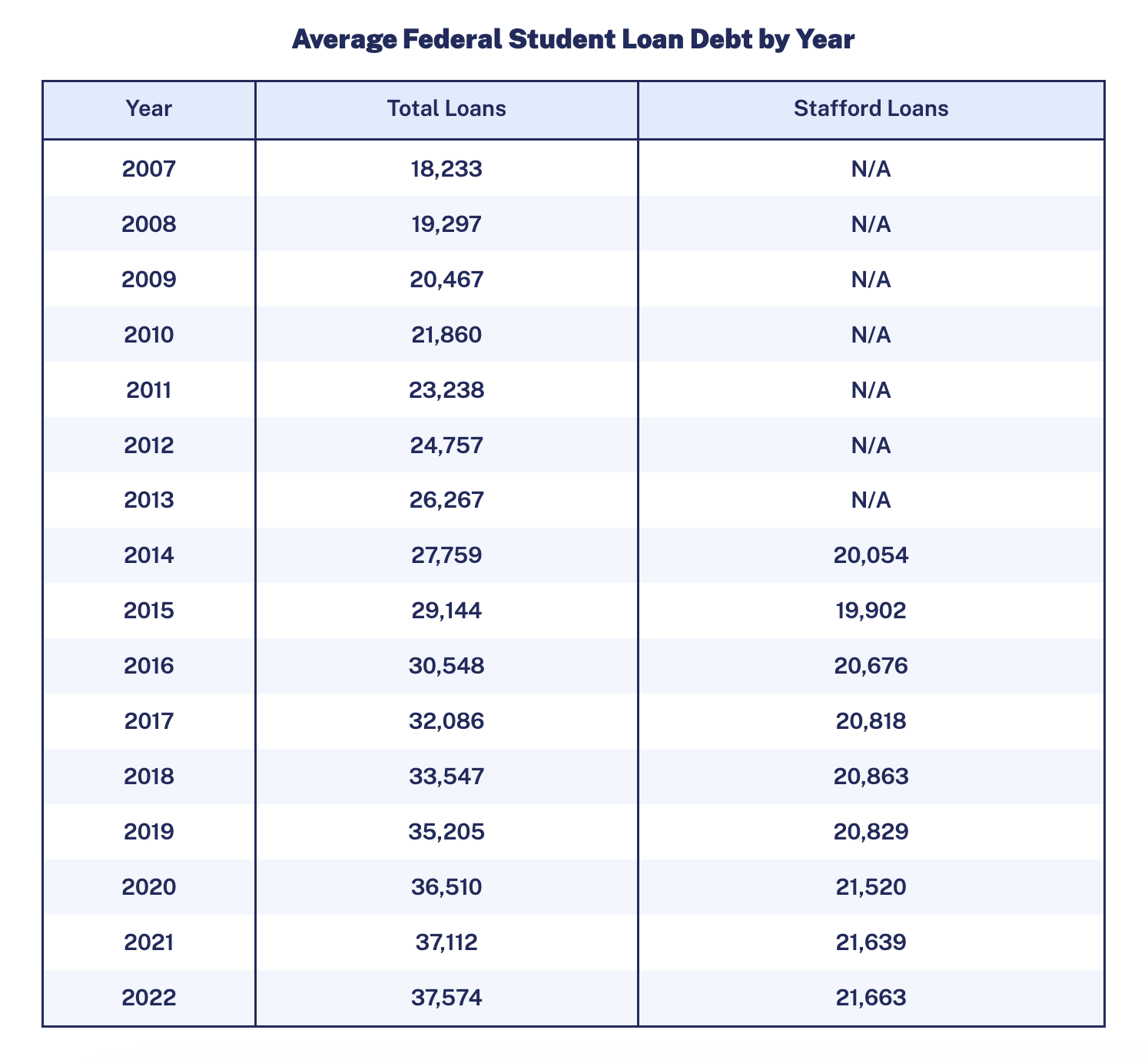

Pupil mortgage debt is a large burden for almost all of American adults. In response to the Training Knowledge Initiative, the common federal scholar mortgage debt is $36,575 per borrower, whereas personal scholar mortgage debt averages $54,921 per borrower.

As of the beginning of this yr, round 45.3 million adults in America have some type of scholar mortgage debt, with a majority of them – 92% – having federal scholar mortgage debt.

Carrying this debt into retirement will not be solely a monetary burden, but it surely takes a pressure in your retirement financial savings plans in the event you do not handle to prioritize these funds.

Taking extra possession of your scholar mortgage debt now will show you how to in the long run, permitting you to direct extra of your monetary efforts later in your life towards establishing your nest egg. In case you’re undecided learn how to handle your scholar loans or have been struggling to make funds, attain out to a monetary advisor for steering, or apply for scholar mortgage reduction help.

In case you at present work within the public sector, or for a authorities entity, see whether or not there are any scholar mortgage reduction applications you possibly can qualify for to assist lighten the burden.

Pay-off your mortgage

Mortgage charges have practically doubled in a yr, because the Federal Reserve continues with its aggressive financial tightening, making it costlier for customers to borrow cash.

In mid-January 2023, the benchmark 30-year mortgage price was 6.48%, up from 3.22% on the similar time a yr in the past. In response to the U.S. Census Bureau, the median month-to-month mortgage cost sits round $1,100.

Individuals have witnessed home costs soar in current months, as demand grows, provide decreases, and the price of labor and constructing supplies proceed to rise.

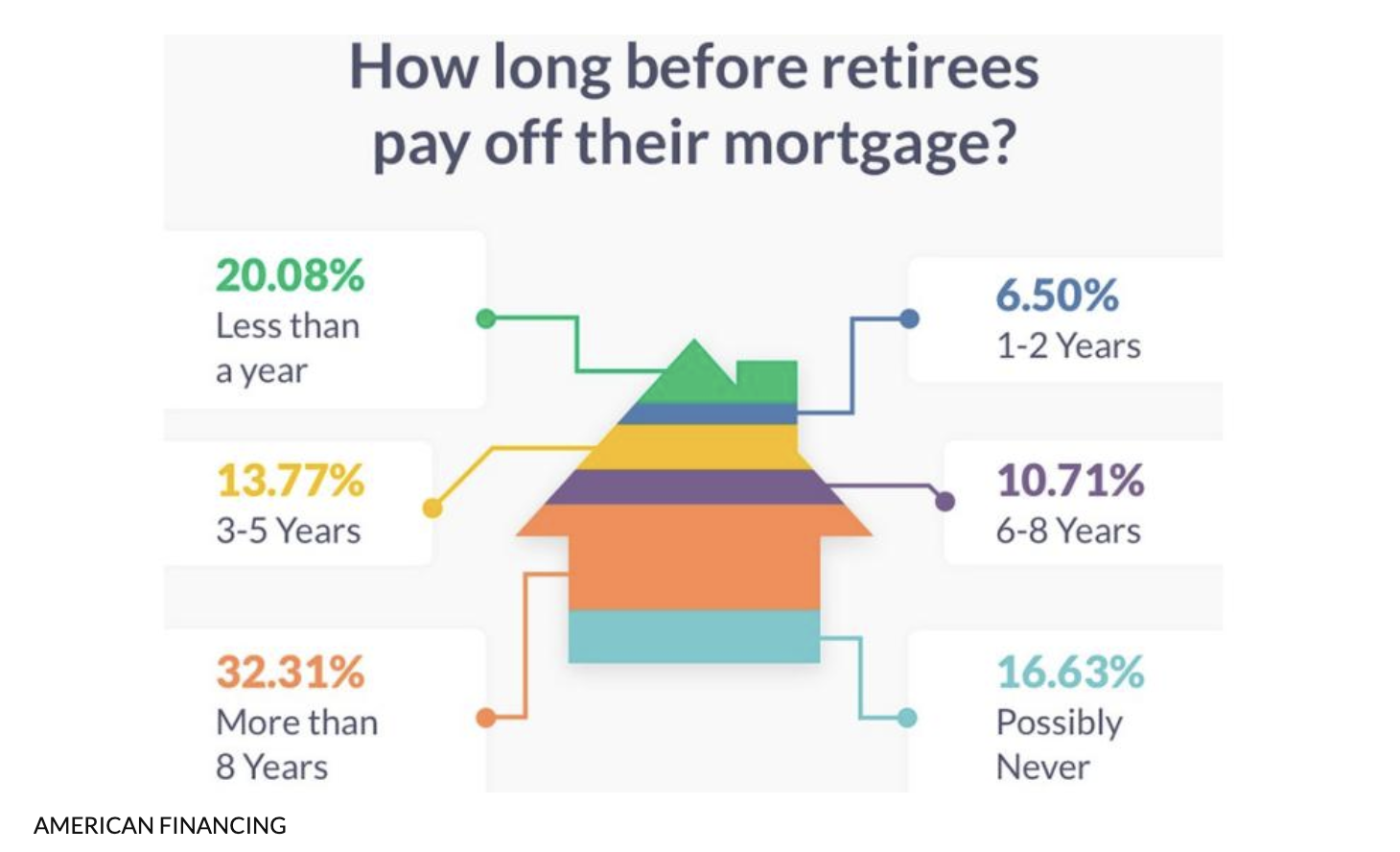

Regardless of these challenges, many adults nonetheless sit with a mortgage by the point they retire. Shockingly sufficient, 44% of Individuals aged 60 to 70 have a mortgage as soon as they step into retirement, with 17% saying they’ll by no means be capable of fully pay it off in line with the American Affiliation for Retired Individuals.

Many soon-to-be retirees and even these nonetheless lively within the workforce live with the excessive cost-burden of their mortgage. Being proactive to cut back these settlements whilst you’re nonetheless pulling a paycheck every month might show you how to decrease your down cost time period, but additionally provide you with some respiration room to slightly put this cash in the direction of your retirement fund.

A number of totally different monetary applications exist to assist householders with fulfilling their mortgage cost duties, and infrequently banks present clear and extra concise monetary steering. Take the chance to resolve these funds sooner slightly than later, and reap the benefits of decrease charges the place potential.

Reassess your automotive insurance coverage

Car insurance coverage tends to extend over time, and insurance coverage suppliers modify funds primarily based on inflation and the market worth of your automobile.

Over time, you could find yourself paying barely extra in your automotive insurance coverage, even in the event you nonetheless have the identical automotive, or maybe have downsized. Values for automotive insurance coverage are calculated by your insurance coverage supplier utilizing the precise money worth (ACV) of your automotive, to find out how a lot they might want to pay out within the occasion of an accident or to conduct any repairs on the automobile.

What some insurers have completed in more moderen instances, is to supply decrease premiums for older clients, to assist lighten the expense burdens they may have on their automobiles. This is able to make it quite a bit cheaper and maybe extra inexpensive for some retirees or automotive house owners to carry onto multiple automotive.

Moreover, you possibly can method your present insurance coverage supplier to assist settle a extra manageable insurance coverage premium primarily based on a number of components reminiscent of years of driving expertise, age, and situation of the automotive, the place it is parked in a single day, how usually you make use of it, and who the first driver of the automotive is perhaps.

These components, together with others will affect the entire month-to-month quantity you will have to pay in your insurance coverage. It is suggested to yearly assess your automobile insurance coverage to be sure you get probably the most budget-friendly deal accessible.

Reduce pointless bills and subscriptions

One other helpful and sensible method to decrease your bills early on in your profession is to keep away from any pointless bills reminiscent of subscriptions, streaming providers, and web payments.

Whereas some might argue that these are important to their on a regular basis way of life and leisure. The most recent figures point out that the common American spends roughly $114 on video downloads and streaming providers, an almost four-figure enhance from 2016.

Web payments have additionally elevated during the last couple of years, regardless of seeing a rising variety of customers coming on-line.

The typical American family pays between $40 and $100 monthly for web providers, with the common being $64 monthly. Even the bottom web packages can price households near $58 monthly when adjusted for taxes and different service charges.

Whereas there’s a want and use for these services or products within the on a regular basis family, it is usually finest to maintain these prices to a minimal. Splitting prices between these residing in the identical home or house could be a technique of bringing down bills.

One other could possibly be to take out fewer streaming or subscriptions and preserve solely the mandatory merchandise which have a goal.

Make sure that to analysis the absolute best offers for most of these providers, and every now and then take a while to assessment your account statements to be able to see the place your revenue is being spent.

You’ll be able to all the time choose out or cancel these subscriptions, however be certain that to learn the nice print first, in order that you do not find yourself paying the next cancellation payment, or proceed paying for one thing you now not use.

The underside line

Planning for retirement has turn out to be a necessary monetary precedence for a lot of Individuals. For people who nonetheless have sufficient time earlier than the age of retirement, it is best to plan and strategize as a lot as potential to make sure you’re on observe together with your monetary and financial savings targets.

Alternatively, for these people which may quickly step out of the workforce, and into retirement, making some cutbacks to attenuate pointless bills, whereas additionally boosting your retirement portfolio is maybe one of the best ways to make sure you can take pleasure in your golden years, with none monetary stress.

There is no proper time to start out saving for retirement, the earlier you’ve got a financial savings plan in motion, the higher. Take management of your funds, and make an effort of breaking down the smaller prices, and decrease prices that would slightly be directed to your retirement fund.

The submit Small Modifications, Huge Outcomes: What You Can Do To Decrease Prices And Plan For Retirement appeared first on Due.