The financial institution runs of mid-March prompted tremors all through the monetary system, and regional banks have been laborious hit.

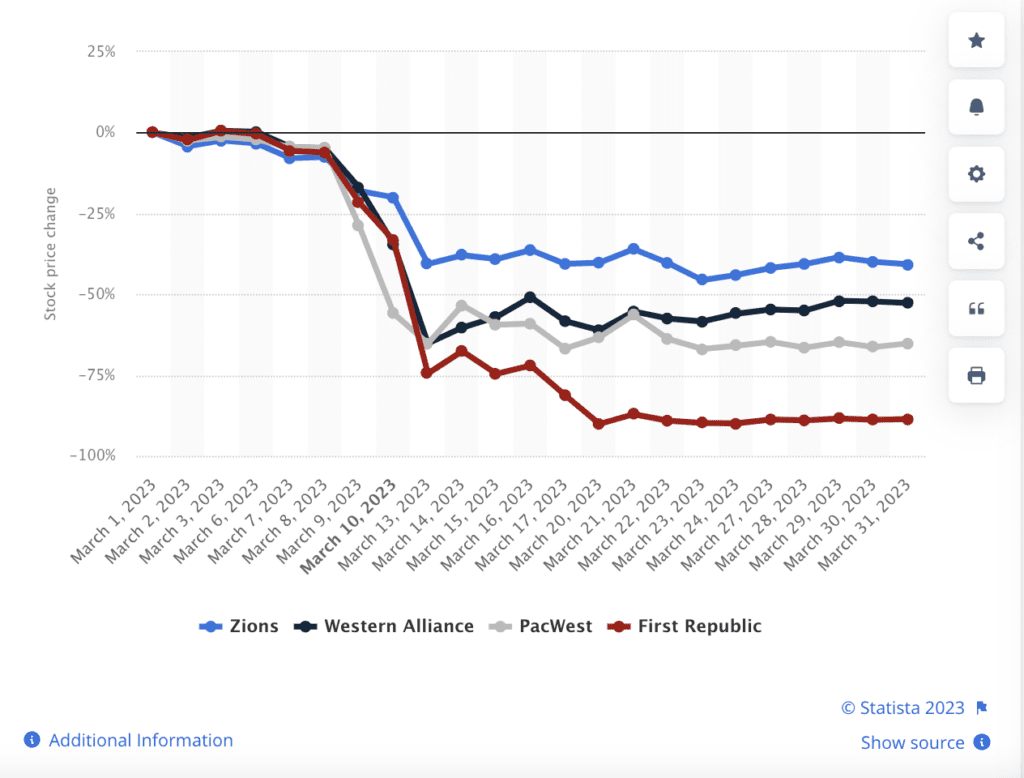

Throughout Silicon Valley Financial institution’s fateful weekend, many main regional banks additionally skilled a nostril dive in inventory costs. They’re but to recuperate. Whereas many leaders now keep that the monetary system is secure, charges have continued to rise, leaving regional banks ever extra weak.

Deposits in US banks totaled $17.1 billion on Friday, Could 10, an additional lower from the week prior. Small banks continued to flounder, with vital bulletins offering slight aid in inventory costs.

This week Pac West, a big supply for analysts’ concern in previous weeks, introduced a sale of its actual property mortgage portfolio, inflicting inventory costs to rally. Their reasoning for the sale was to concentrate on their core group banking enterprise.

Western Alliance, too, noticed a inventory worth bump when final week they reported development in deposits.

However the Regional Banking Indexes nonetheless wallow at a low, KBW down 25% from pre-bank run ranges. Leaders and regulators nonetheless warn of continued strain, with debt ceiling negotiations additional muddying the waters.

Bloating the large banks

Steering the JPMorgan dreadnought, Jamie Dimon has risen because the disaster’ knight in shining armor. In actions echoing 1907, the financial institution, already dubbed “too large to fail,” swooped to the rescue, finally buying First Republic Financial institution and defending depositors from additional upheaval.

Amid the uncertainty, many depositors pulled deposits from regional banks in favor of the large 4. In consequence, JP Morgan introduced a rise in deposits within the first quarter of 2023, amounting to $2.4 trillion.

Whereas “too large to fail” could also be comforting, the shift comes with a trade-off.

“The too-big-to-fail banks serve a useful goal: that your money is secure,” stated Don Muir, CEO and founding father of Arc.

“However these sector banks serve an necessary goal within the expertise ecosystem as a result of they actually perceive the group that they’re serving.”

He defined that bigger banks didn’t have the agility of their regional counterparts, typically focusing as a substitute on solely the massive consumer’s wants. This might imply huge U.S. monetary providers ecosystem areas may stay underserved.

“These banks, Silicon Valley Financial institution, First Republic Financial institution, PacWest, serve the expertise sector. They usually dominate the sector as a result of they perceive these distinctive enterprise profiles burning additional cash than they’re taking in,” stated Muir.

“It’s a disgrace whenever you see the three largest gamers within the offline sector banking ecosystem going out of enterprise…Alternatively, the regional banking system is flawed. You have got sub-scale banks inclined to digital financial institution runs in immediately’s economic system.”

He defined, nonetheless, that the regional banking turbulence could also be the place fintechs may discover a good stronger footing within the monetary providers ecosystem.

Fintechs’ flexibility may give them the sting

Throughout March’s chaos, Arc was one of some fintechs that mobilized to adapt to founders’ must switch uninsured deposits to safer, bank-run-proof places.

The corporate diversifies depositors’ banking stack utilizing banking partnerships, guaranteeing shoppers can have deposits insured effectively over the FDIC $250,000 insurance coverage restrict. In early Could, Arc introduced that they had doubled earlier FDIC protection, amounting to $5.25 million per consumer.

Muir defined their skill to do this was right down to their place as a fintech fairly than a stand-alone financial institution.

“It’s about as secure as doable — most FDIC protection and having a too-big-to-fail custodian associate concurrently. It’s double protection, double safety,” he stated.

He defined that whereas regional banks grew out of a powerful relationship and understanding of their focus market, their small measurement has left them extra weak to financial institution runs. These thought-about “too-big-to-fail” might be shielded from a run on deposits. Nevertheless, their measurement makes an in depth understanding and adaptation to the wants of smaller markets harder to acquire.

Fintechs goal the necessity for customer-centric monetary providers that regional banks have made their area of interest. Being digitally native, with a concentrate on expertise and a capability to adapt shortly, has allowed fintechs to vary in accordance with want a lot sooner than banks of any measurement.

As well as, they will associate with a number of banks if vital, opening them out for partnerships with too-big-to-fail banks and leveraging their security.

“Digital banks can converge the perfect parts of each the regional banking sector and the massive banks, bringing them collectively to serve the economic system,” he continued.

Associated:

Not all hope is misplaced

Nevertheless, some stay hopeful about regional banks’ resilience, and it appears unlikely regional banks will fade into irrelevance with out placing up a combat.

The tempo of deposit flows out of regional banks has declined, and shares appear to be experiencing an uptick.

On Tuesday, Brody Preston, an analyst at UBS, wrote, “No information is nice information for depressed regionals.” He defined that though deposits declined, banks noticed money and different property enhance week over week, implying that throughout the sector, steadiness sheets are in “first rate form.”

The actions of the distressed banks that have been beforehand trigger for concern appear to be working, boosting confidence within the regional banking system.

“Placing all of it collectively, this week’s outcomes present that regardless of the numerous low cost that is still on regional banks, steadiness sheets are largely wholesome and liquid. Single-stock unhealthy information that appears to drive the group on combination are certainly single-stock points on a elementary degree,” Preston wrote.

{kind=link}