The US is among the main nations globally in monetary inclusion, in response to the Precept International Monetary Inclusion Index 2023. Nevertheless, its place is slipping, buoyed solely by developments within the monetary system surrounding debtors’ protections and entry to good high quality fintechs.

Employer Help Broken by Financial Challenges

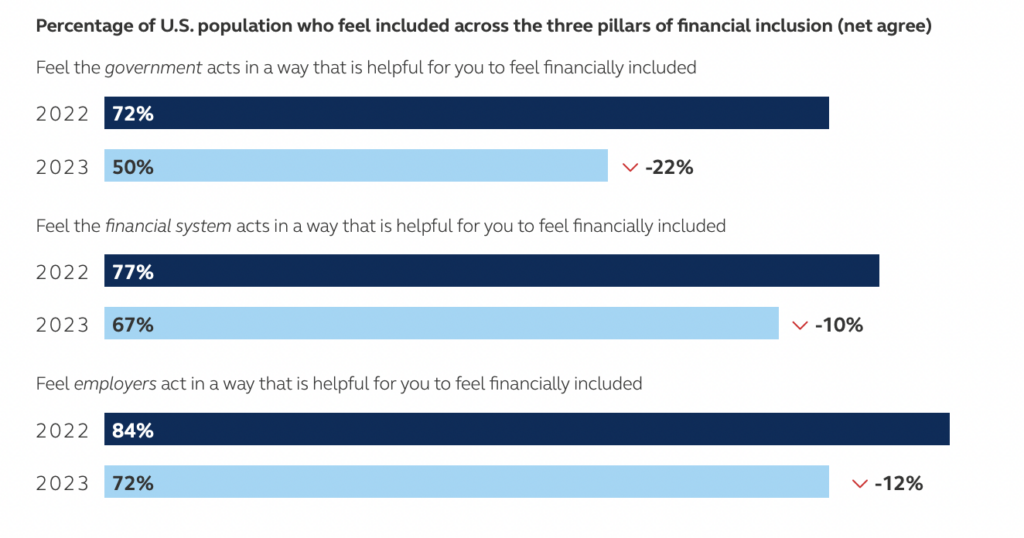

Probably the most vital change was seen within the rating of US employers’ help, which dropped ten positions from being ranked second globally in 2022. Regardless of employers remaining the strongest pillar of help for shoppers to really feel financially included, drops in worker pay initiatives and the availability of help round monetary points had a big impact on the US employer help rating.

“More durable financial circumstances – and associated cost-cutting measures – could also be what’s driving the decrease degree of help reported by US employers within the index,” stated Chris Littlefield, President of Retirement and Revenue Options at Precept Monetary Group.

He defined that the index had famous a decline in employer help correlated with the dimensions of the enterprise. SMEs, making up 99% of US companies, are vital contributors to the employment of the US workforce. Usually underserved by the monetary system themselves, the affect of the deteriorating financial system has made its mark on steadiness sheets, resulting in a tightening of budgets. Bigger corporations with extra sources have been discovered to have the capability for increased worker help, notably throughout difficult instances.

As well as, the US monetary system’s help rating throughout the index solely confirmed two areas of weak point. Each these areas have been centered on declines in help for SME development and enablement of enterprise confidence, mirroring the decline in employer help.

“In an financial downturn, many corporations first look to chop non permanent or contract assist and prices general to assist guard towards job josses,” stated Seema Shah, Chief International Strategist at Principal Asset Administration. “This will likely clarify some od the declines within the Index.”

“Companies taking actions to scale back advantages suggests we’re in the midst of a labor market rebalancing. One of the vital mentioned subjects final yr was wage development as staff have been capable of dictate pay in a decent labor market. As labor markets loosen, the steadiness of negotiating energy usually swings from worker to employer.”

Authorities help didn’t do significantly better than employers when it comes to help, dropping within the areas of economic literacy and consumer-championing rules. Within the eyes of the buyer, the federal government has dropped considerably when it comes to their perceived help. Many felt their entry to monetary merchandise to be restricted and the system itself to be unfair, unable to maintain them into retirement.

Monetary System Robust Catalyst of Monetary Inclusion

Whereas authorities and employer help are sturdy catalysts for monetary inclusion, the index’s research on a world scale confirmed that international locations’ monetary system help had a big impact on their rating. Digital dexterity and developments in on-line connectivity improved monetary inclusion in plenty of creating economies, notably within the Latin America area.

“Bettering on-line connectivity and the event and adoption of digital infrastructure—particularly inside monetary companies—are useful information factors when assessing markets’ development potential,” stated Shah. “These are necessary elements of a financially inclusive society.”

Fintechs appear to play a big function in bettering the help of economic inclusion due, partially, to their digital-native make-up. Quoting the World Financial institution’s International Findex, the Precept index said that the evolution of fintech has been essential to accelerating monetary inclusion worldwide, particularly in creating markets.

Within the UK, with enhancements within the finance sector to allow SME development, common enterprise confidence, and rising the presence of fintechs, the nation improved its rating by seven locations. Within the case of the US, regardless of drops in each authorities and employer help, the nation’s rating remained excessive as a result of sturdy help of the monetary system.

Nevertheless, the US nonetheless faces challenges to monetary inclusion, and its slipped rating is at risk of falling additional. Fintech improvement and digital infrastructure might be key in retaining their lead.

“Monetary exclusion is an actual drawback for possibly as a lot as a 3rd of america,” stated Jason Capehart, Head of Information Science and Machine Studying Engineering at Mission Lane. “Know-how and inclusiveness from an information perspective is of the ways in which we will strategy that drawback and enhance it.”

“What fintechs do as an business is use methods to enhance that and supply companies, particularly when you consider transferring past a few of these walled gardens of the legacy monetary companies system.”

Trying to information as a driver of US Monetary Inclusion

Feeding into fintechs potential to make use of various information lies the federal government help. The index confirmed that the US authorities help pillar had dropped in its world rating, dragged down, partially, by a lower within the rating of consumer-championing rules.

Nevertheless, in October 2023, the CFPB proposed the Private Monetary Information Rights rule geared toward bettering shopper management over information sharing in a bid to speed up open banking. If handed, the rule would shield clients from “dangerous” information assortment practices similar to display scraping and permit them to rescind entry to information in addition to share information with third events as wanted.

The regulator has additionally initiated analysis into the usefulness of money circulate information in underwriting. In July 2023, the CFPB said that “Cashflow information could assist lenders higher establish debtors with low chance of significant delinquency, even when these debtors’ credit score scores could have in any other case prevented them from receiving credit score.” Whereas they said that extra analysis was wanted, it gave weight to an space fintechs had been addressing for years.

“It offers us methods of offering an understanding of what somebody’s credit score threat or monetary well being is in ways in which merely weren’t widespread follow a decade in the past,” stated Capehart. “The issue that a whole lot of Individuals run into is that they don’t seem to be a part of the normal prime or upper-class monetary system.”

“With the ability to pull issues in like open banking information, and money circulate, underwriting information, give monetary establishments the power to grasp who their clients are, and the way they make their funds work and the way they make ends meet.”

He defined that whereas regulation was a superb factor, the realm was sophisticated. Regulators run a threat of incurring unintended penalties that would affect shoppers negatively.

“But when we get it proper and discover methods of selling transparency in information and permitting individuals to maneuver and consider, permitting shoppers to judge their choices, by making their information moveable, there’s this nice alternative for enchancment and competitors that you just simply didn’t have earlier than.”

{kind=link}