Like many others, UK Cost Service Suppliers (PSPs) have felt the squeeze of the difficult financial system. Previously six months, its results have rippled throughout the sector, resulting in heightened fraud, enterprise prices, and a wave of misplaced clients. Improvement in Open Banking may very well be key.

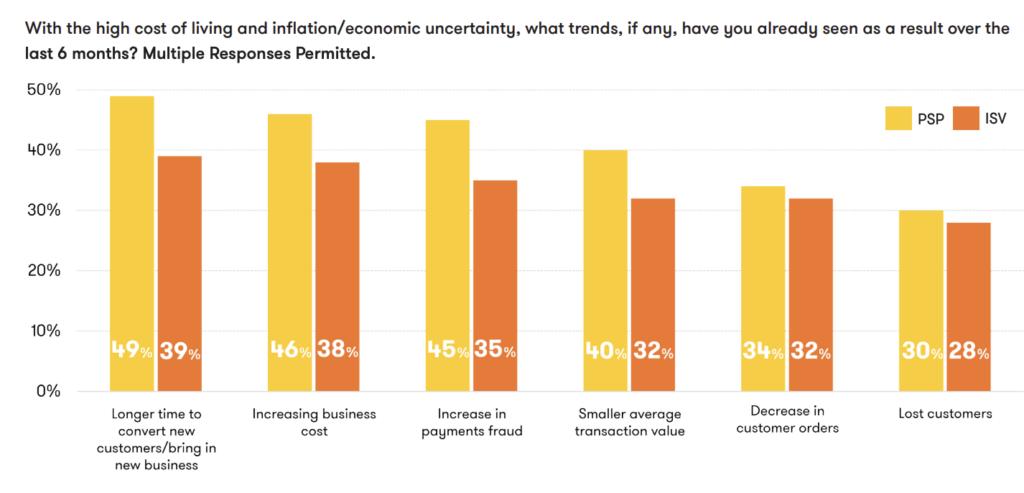

In response to a research performed by EML and Nuapay, each single one of many 250 fee professionals surveyed famous an affect of the price of residing disaster on their enterprise. Nearly half of all PSPs surveyed reported longer buyer conversion instances and declining transaction values. Their results had been compounded by heightened enterprise prices brought on by ongoing provide chain disruption, labor shortages, and elevated vitality prices.

“The enterprise challenges confronted by PSPs and ISVs may probably threaten funds innovation if headcount is lowered or income drops additional,” stated Ruwani Hewa, Product and Propositions Director, Nuapay. Over the previous few years, specifically, revolutionary fee applied sciences have been a vibrant spot amid uncertainty, supporting the event of digital economies and maintaining cash transferring. PSPs and ISVs have performed an important position right here, and it’s necessary that we proceed to assist them.”

Along with the cost-of-living pressures, 45% of PSPs famous a rise in funds fraud. The Robust Buyer Authentication (SCA) rules, launched in 2019, had been meant to focus on fraud ranges and make on-line funds safer. As a substitute, it has added elevated friction to checkouts, and 70% of PSPs have seen checkout abandonment enhance by 41-100%, including to the declined charges of buyer transactions.

“It’s clear that SCA rules haven’t been the silver bullet that regulators hoped they’d be. As a substitute, they’ve created critical checkout friction for shoppers paying by card and – crucially – misplaced gross sales for companies,” stated Brian Hanrahan, CEO of Nuapay.

“Nonetheless, with Open Banking funds, the consumer expertise is way improved, with authentication already embedded on cell. For example, with Open Banking, shoppers can use biometrics to immediately confirm and approve funds.”

Improvement Of Open Banking More and more Necessary

Within the face of those elevated challenges, many contemplate Open Banking to retain vital potential in bettering the circumstances for PSPs. Nearly half of PSPs within the Nuapay research famous that built-in fee applied sciences like open banking are important to stay aggressive.

“There’s no fast treatment to the enterprise challenges confronted by the retail sector, however expertise has indicated that perfecting the funds course of is integral to rising buyer loyalty, lowering basket abandonment, and opening new income streams,” stated Hanrahan. “Adoption of Open Banking can assist the retail sector and its enablers, together with PSPs and ISVs, by means of a really difficult interval.”

“Open Banking is a less expensive different to conventional fee choices, bypassing costly and inefficient rails that include hefty third-party charges,” Hewa added. “Not solely does investing in Open Banking expertise imply that retailers can decrease charges, however it additionally improves cashflow, as funds are settled in real-time.”

The Open Banking sector within the UK is presently rising at a price of 10% month-over-month as extra are recognizing its advantages. Nonetheless, with solely 9.5% of shoppers and SMEs utilizing Open banking providers in January 2023 and solely 10% of shoppers stated to be recurrently energetic customers, the sector has a option to go but for mass adoption.

RELATED: UK nabs prime spot in open banking league desk

The Impact of Elevated VRPs

Many PSPs see improvements like Variable Recurring Funds (VRPs) and Request to Pay (RtP) driving the adoption of Open Banking ahead.

VRPs use open banking to allow customers to arrange approved funds of variable quantities to be taken out of their accounts with trusted PSPs. The innovation is claimed to assist with friction and ease of funds, significantly for subscription purchases, changing the necessity for direct debits.

RtP has related advantages, however as a substitute of a direct recurring fee being approved, retailers ship a request to the shopper for fee, and the shopper can select to simply accept, decline, or pay partly.

Whereas PSPs see the potential for its utilization, many famous {that a} lack of training in retailers and clients as to the advantages of the fee technique had blocked vital adoption. A standardized framework for VRPs was additionally but to be established, regardless of the PSD2 framework being established for over 5 years, creating frustration amongst PSPs.

“VRPs have the potential to gasoline the subsequent stage of Open Banking adoption. Nonetheless, the trade wants a standardized framework for this to occur,” stated Hanrahan.

Whereas the Joint Regulatory Oversight Committee (JROC) introduced its give attention to the event of a VRP framework earlier this yr a pilot is just not projected for an additional two years. Within the meantime, PSPs have seemed to the non-public sector for options.

RELATED: CFPB Proposes Rule to Speed up Open Banking

{kind=link}