{kind=link}

As information of a sustained inflation charge within the UK surpassing a lot of Europe, the price of dwelling disaster turns into ever extra entrance of thoughts.

Battling by means of months, which have changed into years of difficult circumstances, UK households proceed to wrestle with out a lot respite. The toughest hit is these with restricted entry to monetary providers.

In Plend’s current Monetary Inclusion Report, the corporate constructed on its findings surveyed within the wake of COVID to measure the impression of the price of dwelling disaster on the underserved.

“For what was already a troublesome panorama for many people with skinny and inaccurate credit score recordsdata (presently holding again over 20 million adults within the UK based on analysis by PwC), the scenario has now been exacerbated by rising vitality, meals, and housing prices,” mentioned Robert Pasco, Co-Founder, and CEO of Plend within the introductory notes of the report.

“These erode our capacity to entry reasonably priced mortgages, inexperienced house enhancements, and debt consolidation options.”

Worsening circumstances and elevated vulnerability

The report discovered that, unsurprisingly, there continues to be misery amongst respondents, with 49% reporting a adverse impression on their bodily and psychological well being. The worsening circumstances for the reason that pandemic has brought about growing numbers of individuals to wrestle to repay loans and acquire entry to credit score merchandise.

Throughout UK households, common bank card debt had shot up, the report discovering a rise of £1,774 in common bank card stability between 2022 and 2023. Nearly 30% of respondents mentioned they used their bank cards greater than as soon as every week. BNPL stability had additionally practically tripled within the final yr.

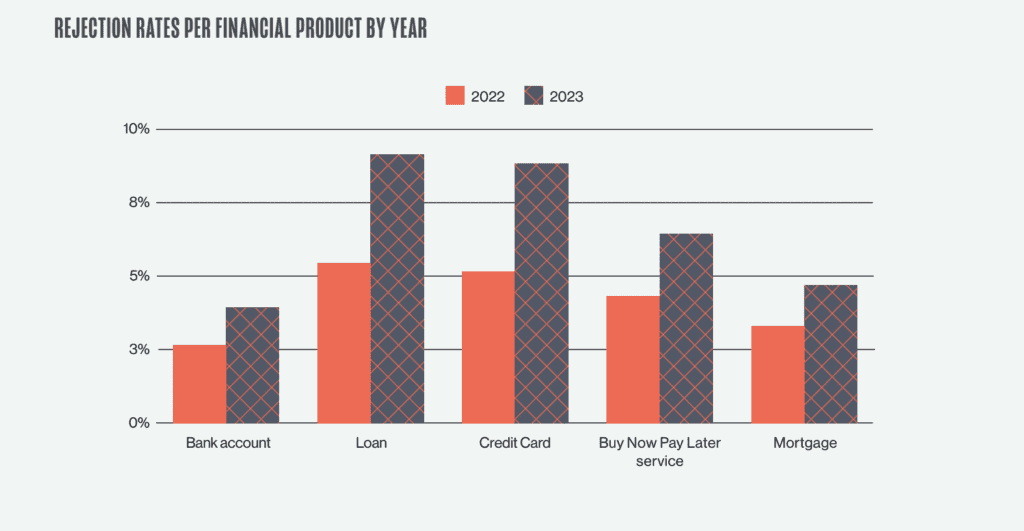

Regardless of the rising want for credit score merchandise, rising charges have made them much less reasonably priced. As well as, Plend discovered that total rejection charges have elevated over the previous yr for credit score merchandise, notably for loans and bank cards.

“Current StepChange analysis revealed that the price of dwelling disaster has led to greater than two in 5 UK adults (43%) taking motion akin to rationing day-to-day requirements together with vitality, meals, and housing prices, lacking important payments, or counting on assist from pals or household to maintain up with credit score repayments,” mentioned Richard Lane, Director of Exterior Affairs at StepChange Debt Charity.

“For these counting on credit score to make ends meet, it’s possible that borrowing to cowl the fundamentals will solely exacerbate the monetary issue.”

It was reported that a minimum of 17.5 million folks within the UK are thought-about financially susceptible, with one in eight households estimated to expertise a minimum of one kind of poverty premium. Rising ranges of respondents felt “locked out” of the monetary system, notably these from black and minority ethnic backgrounds and youthful generations.

Most of those teams mentioned they’ve turned to sources of credit score to tide them over the troublesome interval.

As a consequence of their incapability to entry regulated credit score, many have turned to family and friends and unlawful sources akin to mortgage sharks. Plend discovered that 3% of the UK grownup inhabitants has used a mortgage shark within the final 12 months, and lots of are actively contemplating utilizing one.

Mortgage shark utilization is reportedly far higher amongst those that are already susceptible to the consequences of monetary exclusion and the price of dwelling disaster. This may end up in a number of points, akin to threats of violence and psychological manipulation, piling growing strain on these teams and exacerbating the problems posed by the price of dwelling disaster.

“In January 2023, the ONS5 discovered that 15% of UK adults reported that they’d wanted to make use of credit score greater than standard, with households with dependent kids and those that pay for gasoline and electrical energy by means of prepayment meters much more prone to be doing so,” mentioned Sara Davis, Senior Analysis Fellow on the Private Monetary Analysis Centre at Bristol College.

“Due to this fact, whereas addressing insufficient revenue and offering monetary help is most necessary, making certain that households have entry to reasonably priced and honest credit score is a right away concern.”

Cross-industry strategy essential

Plend argues that in mild of the findings, the UK inhabitants hangs in a essential place that may very well be eased by a number of stakeholders reviewing their approaches to credit score merchandise.

“Entry to reasonably priced credit score is significant for a person’s monetary stability and psychological well-being. Nevertheless, this report exposes that giant sections of the UK inhabitants are repeatedly being let down,” wrote Pasco. “As a consequence of the price of dwelling disaster, establishments, lenders, and banks are wrongly taking benefit by charging charges in extra of the Financial institution of England base charge will increase to this point.”

The report concluded with an overview of a method calling {industry} actors and authorities officers to enhance important areas of accessing credit score. Transparency on rates of interest and lowering bias by means of “blind credit score functions” drastically enhanced the general public’s understanding of credit score merchandise and their capacity to be accredited.

The corporate additionally known as upon authorities officers and policymakers to enhance training about unlawful lending and implement monetary inclusion requirements.

“A collective effort from each {industry} and the regulator is required to make sure a extra equitable and accessible monetary panorama for the UK inhabitants,” mentioned Alice Tapper, Monetary campaigner and Head of Influence at Plend.

“Important to enabling this motion is the prioritization of those points by the federal government, adopted by a powerful legislative response. The compounding results of the COVID-19 pandemic and the continuing price of dwelling disaster threaten to scar the monetary lives of numerous people, making well timed and decisive intervention all of the extra essential.”

RELATED: Value of dwelling disaster essential: UK fintech sector mobilizes

-

Isabelle is a journalist for Fintech Nexus Information and leads the Fintech Espresso Break podcast.

Isabelle’s curiosity in fintech comes from a craving to know society’s speedy digitalization and its potential, a subject she has typically addressed throughout her educational pursuits and journalistic profession.