“Superior AI may symbolize a profound change within the historical past of life on Earth,” said the Asilomar AI Rules in 2017, two years after the founding of OpenAI.

Quick ahead to 2023, and its results are already being acknowledged.

The introduction of generative AI into the tech ecosystem has opened out realms of alternative, beforehand thought solely to be the stuff of fiction. From chatbots to monetary forecasting, the applying of the know-how is being each revered and feared, with even the founding fathers of Open AI calling for a pause in growth.

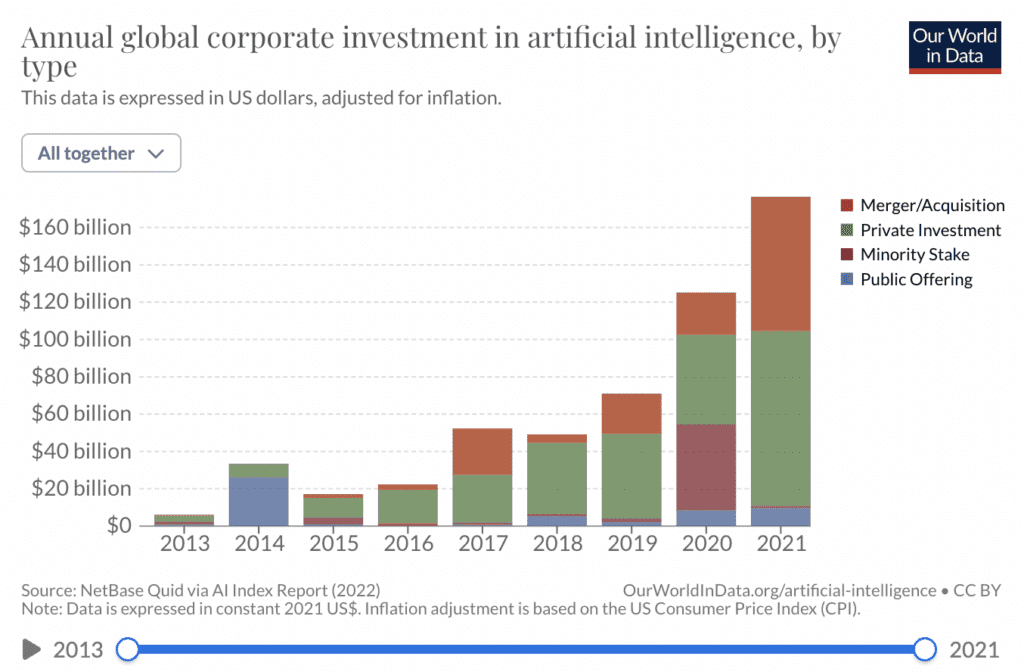

Regardless of the considerations, the advantages of the know-how are paralleled by few, and traders have seen. AI market measurement is anticipated to achieve $407 billion by 2027 (from $87 billion in 2022), and 83% of companies have made AI their high precedence.

Generative AI to streamline lending

Whereas AI has touched many areas of monetary companies, lending has seen vital innovation.

Ocrolus, a enterprise targeted on doc automation and a companion to many digital lenders, has used AI since its inception in 2014. The corporate introduced earlier this month that they had been taking their utilization a step additional, integrating OpenAI GPT (generative pre-trained transformer) embeddings.

“It helps with contextualizing info from more difficult paperwork,” stated Sam Bobley, Co-Founder and CEO of Ocrolus.

He defined that the corporate had used Optical Character Recognition (OCR) AI for a number of years, utilizing know-how from Google and Amazon. That they had additionally applied their very own machine studying infrastructure to achieve a excessive degree of doc recognition and streamline lenders’ doc studying course of for underwriting.

Associated:

The mixture of the three options had allowed Ocrolus to course of paperwork effectively, permitting their shoppers to deliver mortgage descisioning instances to a matter of hours.

As well as, the corporate makes use of human intervention to verify errors in doc evaluation.

“The key sauce for Oculus, one among our greatest differentiating components is we do software program, however we even have our crew of Oculus high quality management professionals to verify all the information output is completely clear earlier than it goes again to the client,” stated Bobley.

Though beginning with small enterprise loans, the corporate had set its give attention to the difficult mortgage utility course of. This expertise allowed them to department out to different markets, comparable to rental functions and private loans.

“If you are able to do all the paperwork within the mortgage packet, it’s very complete,” he continued. “It’s allowed us to start out enjoying in these different asset courses.”

Standardized formatting problem

Though Ocrolus had already lowered doc evaluation instances from days of labor to a matter of minutes, Bobley defined that in some cases, the unique AI techniques had discovered it difficult to investigate paperwork that don’t have a standardized format.

“The toughest a part of the job is contextualized info from varied codecs,” stated Bobley. “A number of the know-how that Open AI has constructed is superior at that contextualization effort, in comparison with among the different OCR suppliers on the market.”

“For instance, pay stubs can come from a whole bunch of hundreds of various payroll techniques within the nation that produce completely different codecs. There are 5,000-10,000 banks, credit score unions, and group banks.”

He stated that the generative AI from OpenAI may learn the paperwork precisely regardless of the differing codecs, a job which will have beforehand wanted enter from a human workforce.

The result’s a capability to scale back the variety of faulty paperwork despatched for human evaluation, lowering total doc evaluation instances even additional. It additionally opens out the software program for varied different information sources.

“All fintech lenders are already utilizing different information,” stated Bobley. “I feel banks and mortgage lenders are additionally beginning to look extra significantly into these information sources. We give lenders the power to retrieve that information a lot sooner and extra precisely and ship it immediately into their very own back-office credit score scoring techniques.”

{kind=link}