{kind=link}

As we transfer by months of dropping valuations and funding rounds, the temper could also be somber within the fintech group.

In response to a brand new report carried out by QED Buyers and Boston Consultancy Group (BCG), since April 2022, valuations have dropped across the globe by 60%.

Whereas early-stage firms nonetheless see some funding, the extra mature the enterprise, the tougher it has turn into to fundraise. Rising charges have made their mark, and with Jerome Powell, Chair of the Federal Reserve, asserting even additional hikes yesterday, concern ripples by the business.

Nonetheless, the report devoted only some paragraphs to this previous yr’ blip, stating that it may characterize solely a short-term correction.

“Basically, we’re witnessing a shakeout and tempering of enthusiasm for growth-stage firms which have unclear product and/or market matches…A few of this filtering is nice for the business, as weaker enterprise fashions have gotten confused and successfully being weeded out,” the report learn.

The difficult surroundings has brought about fintech leaders to shift their focus, shifting from progress at any price to strengthening fundamentals – a transfer that might work wonders for the years forward, rising sixfold from $245 billion to $1.5 trillion by 2030.

Nonetheless ripe for disruption

Fintech turned a disruptor to the monetary providers business, an space QED and BCG really feel continues to be fertile for disruption.

“This report highlights one thing that, anecdotally, QED has witnessed firsthand: that fintech’s story is in Chapter 2, not Chapter 8, and that a lot of this highly effective narrative continues to be to be written,” says Nigel Morris, Managing Accomplice of QED Buyers and coauthor of the report.

“Fintech sits inside monetary providers, which is an enormous, worthwhile business, and the chance forward of us to democratize entry to those providers on a world scale is super.”

The report said that the monetary providers business is without doubt one of the most worthwhile segments of the worldwide economic system. It represents $12.5 trillion in annual income swimming pools and creates an estimated $2.3 trillion in annual internet income.

Nonetheless, many points nonetheless exist the place fintech may make a major influence.

“The fintech journey continues to be in its early phases and can proceed to revolutionize the monetary providers business as we all know it,” says Deepak Goyal, Managing director and senior associate at BCG and co-author of the report.

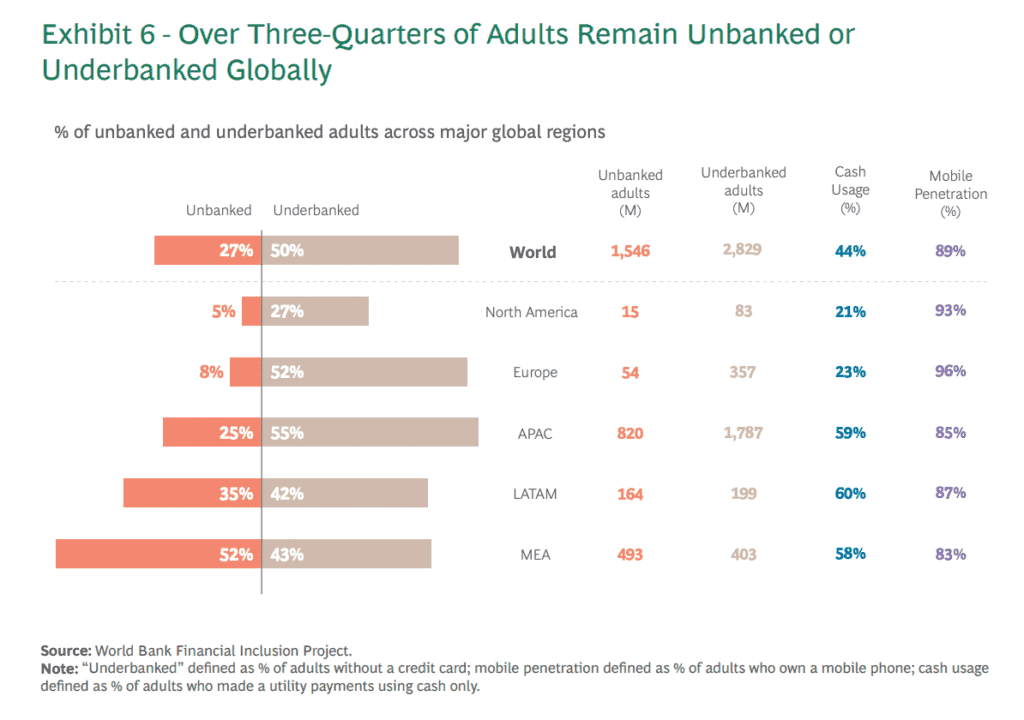

“Buyer expertise stays poor. Over half the world’s inhabitants stays unbanked or underbanked, and know-how continues to unlock new use circumstances in leaps and bounds. All stakeholders should due to this fact seize the second. Regulators should be proactive and lead from the entrance. Incumbents ought to associate with fintechs to speed up their digital journeys.”

New applied sciences are but to have their full influence

To deal with persevering with points, know-how has been consistently evolving. Rising applied sciences, crammed with potential, have entered the fintech house to spark new approaches or strengthen present ones.

The report singled out generative AI; API-based open connectivity; DLT; quantum and edge computing; and embedded-hardware Web of Issues (IoT) and biometrics as having essentially the most potential within the fintech house.

Generative AI is a buzzword now acquainted to many. Whereas at present gaining headlines as a toy of dystopian science fiction, the know-how is seen by QED and BCG as a device that might go far past supercharging customer support. In response to the report, it “will support incumbents by serving to them leapfrog their technical constraints,” combatting fraud, boosting safety, facilitating “monetary concierges, ” and streamlining labor-intensive industries.

API-based open connectivity, or “open banking 2.0,” may even have vital outcomes. Already the advantages of opening out entry to monetary info have impacted fintech. Its continued improvement may strengthen international interplay between monetary establishments and enhance their strategy to fraud, underwriting, and threat evaluation.

Blockchain and Distributed Ledger Expertise (DLT) are already making waves in monetary establishments, with many constructing infrastructure regardless of a cool-down in crypto. Worldwide the know-how might be utilized to worldwide settlements making a platform that’s predicted to be quick, cheap, and safe, eliminating intermediaries utilizing sensible contracts. These attributes may give beginning to new and streamlined providers and monetary instruments. The tokenization of complicated real-world belongings and the regulation of digital belongings proceed to be key to unlocking their potential.

Quantum and Edge Computing, whereas the “subsequent large factor” for fairly a while, keep their potential as formidable instruments when utilized to monetary providers. With the power to course of vital quantities of information, the know-how may optimize processes and tremendously affect approaches to fraud and underwriting.

Embedded-{Hardware} IoT and Biometrics can be utilized to streamline and personalize monetary merchandise. IoT’s networking functionality permits info to be despatched to and obtained from web gadgets, equivalent to kitchen home equipment and smartwatches. It might be harnessed to affect insurance coverage and customized loans. Facial recognition can streamline checkout experiences.

Onward and upward

Given the potential for rising applied sciences, monetary establishments may discover methods to serve clients far past the present scope.

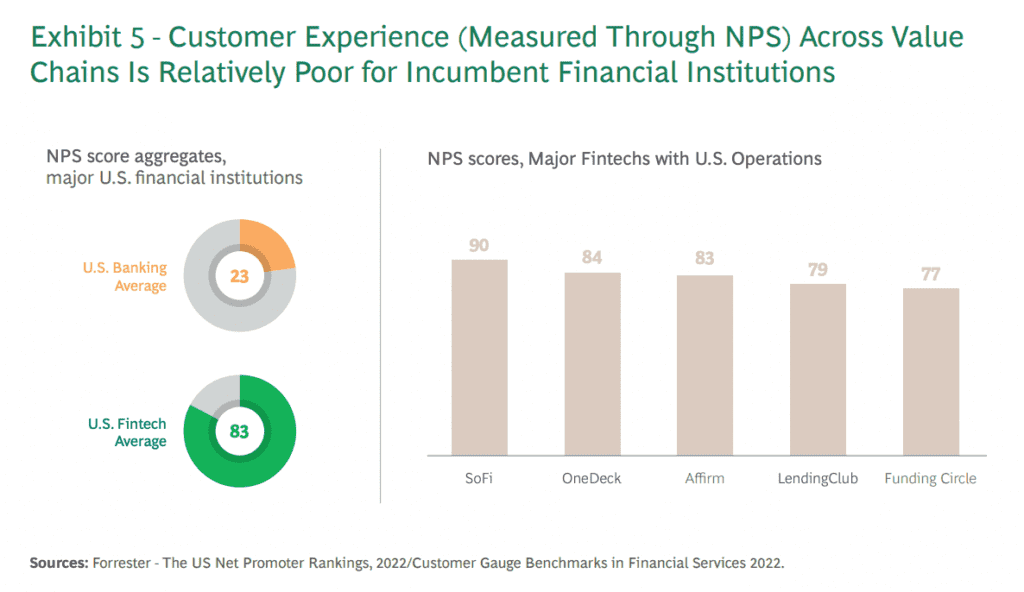

Fintech has been uniquely positioned to focus on poor customer support. In monetary providers, a sector that continues to have low Internet Promotor Rankings, the common rating of fintechs greater than triples that of banking.

As well as, over three-quarters of the worldwide inhabitants stays unbanked or underbanked. Whereas the degrees in North America are the bottom, Asia, LatAm, the Center East, and Africa, all present vital potential but to be addressed.

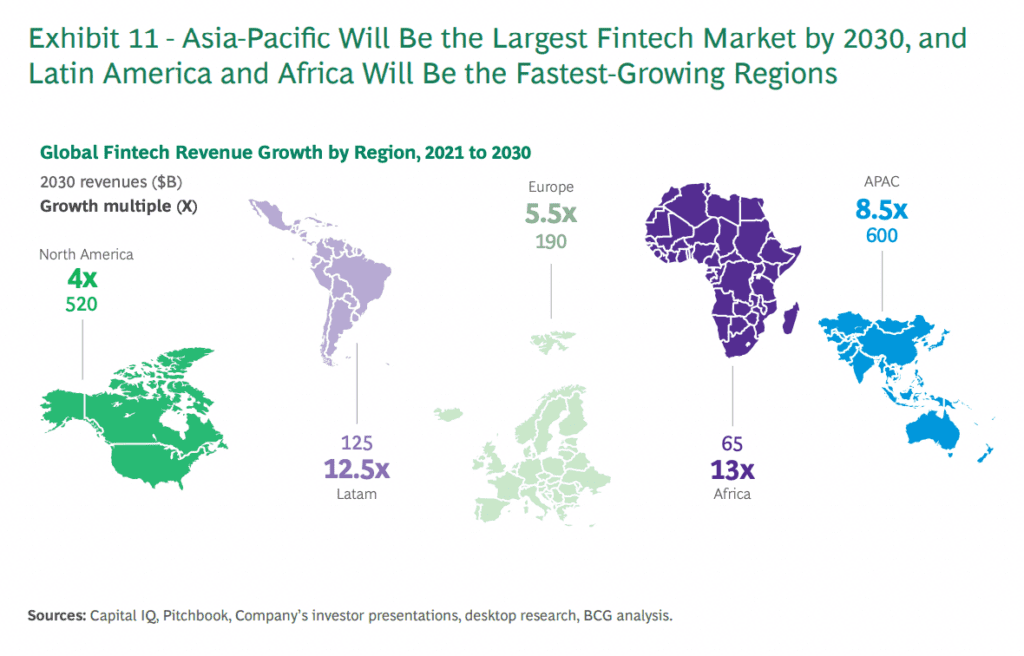

North America, the forerunner for now, generates a lot of fintech’s international income, adopted carefully by Asia-Pacific (APAC). Nonetheless, APAC continues to be an underpenetrated marketplace for fintech, with nearly $4 trillion in monetary providers income.

The report predicted that by 2030, APAC would have overtaken North America as essentially the most distinguished fintech market, with a projected compound annual progress price of 27%. They felt that a lot of this progress could be pushed by native entities, fixing entry points and driving monetary inclusion.

A lot of the expansion is predicted to come back from China, India, and Indonesia, addressing the huge volumes of underbanked populations and excessive numbers of SMEs. Already leaders within the improvement of tremendous apps, China is predicted to guide APAC’s progress in fintech. India’s vital fintech exercise, sympathetic regulatory regime, and shifts in demographics and GDP make it a formidable participant.

North America continues to be predicted to develop considerably, accounting for 32% of worldwide fintech income by 2030. That is anticipated to be pushed primarily by B2B and B2BX options, the enlargement of fintechs to incorporate extra providers and the nation’s interchange pool. Open banking has but to take maintain, doubtlessly sparking elevated innovation totally.

Europe may also see continued progress, supported by regional enlargement. The report highlighted the impact of supportive regulation, boosting income by 21% between 2023 and 2030. Right here, too, open banking is predicted to have a major influence.

As well as, LatAm and Africa are prone to see the quickest progress. Whereas now, fintech penetration is already growing; it’s predicted to speed up, attracting worldwide funding whereas experiencing rising adoption of unbanked and underbanked populations.

Brazil, particularly, with its manufacturing of business gamers equivalent to Nubank and Creditas and programs such because the PIX on the spot fee system, is prone to spur this progress.

Associated:

The report predicted a “leapfrogging” of African and Center Jap incumbents, innovating to draw a tech-savvy inhabitants, significantly in smartphone-based options.

Not with out stipulation

Nonetheless, this anticipated progress is conditional, and the report warns that dangers and uncertainties stay.

Regulation is seen as a sticking level the place a steadiness should be struck to foster ongoing innovation and adoption. The report learn, “The long run progress of fintech would require regulators to behave with urgency and thoughtfulness extra holistically,” shying away from the reactionary strategy of yesteryear.

Belief can also be a major issue, and it was said that the business faces reputational dangers that might compound. Knowledge leaks had been an space particularly that might trigger harm to buyer loyalty and ongoing adoption.

In addition to this, the danger of bigger incumbents with deep pockets within the face of a difficult funding surroundings may stifle progress by anti-competitive practices. “There are primarily 4 teams of stakeholders within the fintech universe: regulators, fintechs themselves, incumbents, and traders,” the report said.

“The expansion and success of the fintech sector will rely largely on how these 4 stakeholders can work collectively for the long-term good thing about the worldwide monetary providers sector and the billions of consumers it serves.”

12 distinctive views, 12 distinctive views in the present day

-

Isabelle is a journalist for Fintech Nexus Information and leads the Fintech Espresso Break podcast.

Isabelle’s curiosity in fintech comes from a craving to know society’s speedy digitalization and its potential, a subject she has usually addressed throughout her tutorial pursuits and journalistic profession.