VC funding had already met a chilly snap. In March 2023, when Silicon Valley Financial institution (SVB) met its demise, the start-up neighborhood had endured months of downrounds. Funding was scarce, and fairness was costly. Enterprise debt was seeing its quickest comparative progress in years.

Then SVB collapsed, adopted by Signature and First Republic, a number of the main banks serving the startup neighborhood. The results have been felt by lots of their friends, wiping out an estimated 70% of enterprise lending.

The impact on the VC house was catastrophic. The primary half of 2023, already dealing with drops in deal quantity, noticed it plummet. Pitchbook’s enterprise monitor registered a 38% drop in enterprise debt deal rely of Q2 2023, with offers for early-stage start-ups dropping by virtually 50%.

All at a time when demand was reaching report highs for the last decade.

After a brief interim, SVB returned to the enterprise debt house, now beneath the care of First Residents. However its mortgage e-book was broken together with its popularity, and credit score requirements throughout the banking trade had tightened.

Whereas the banks failed, different firms stepped in, performing as first responders to the disaster dealing with the startup neighborhood. As we speak, Arc, one of many fintechs on the entrance strains of the SVB disaster, has launched a enterprise debt facility to satisfy the rising demand.

RELATED: Submit SVB sale, VCs transfer to sustainable progress

Assembly the Provide/Demand hole for Enterprise Debt

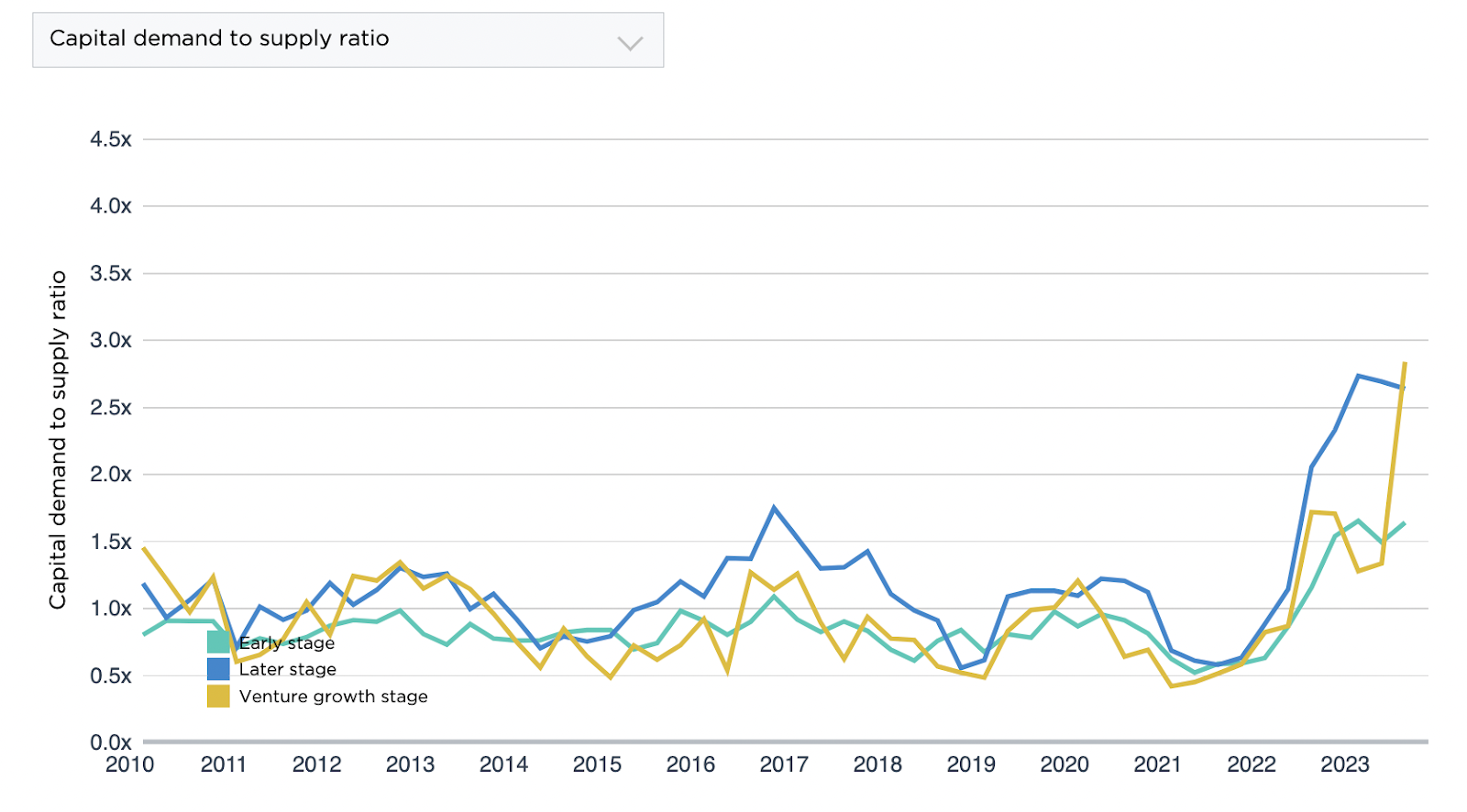

“Within the months since SVB’s crash, we’ve seen a pullback in enterprise lending by the banks, regional banks, nationwide banks, and GSIBS. However with elevated demand,” mentioned Don Muir, Co-Founder and CEO of Arc. Pitchbook locations present demand at shut to a few instances the quantity of provide for the enterprise progress stage and later funding, with a robust indication it’s more likely to proceed rising.

“There’s an even bigger hole in provide and demand than there’s been for years. It’s fairly stark…founders don’t know the place to go.”

Muir defined that on this setting, startups are dealing with two choices to fund their progress. “You may both not increase enterprise debt and lift solely fairness, due to this fact incur an incremental 20- 30% of dilution alongside your spherical. Otherwise you exit and attempt to discover a completely different lender.”

“However the actuality is, the entire lenders, alongside SVB’s crash, they pulled again. And credit score funds they moved in, however they’re priced wider than SVB. And startups have issue stomaching funding from these firms.”

Muir defined that whereas the supply of capital had turn out to be scarce, startups had turn out to be extra environment friendly and resilient to the downturn, making many glorious candidates for longer-term financing. Following Arc’s income financing choices for startups, the enterprise debt resolution offers longer-term capital for startups trying to fund progress.

He mentioned that by means of Arc’s expertise processing credit score transactions for short-term financing, Arc had amounted to information to create environment friendly underwriting fashions that would now be utilized to longer-term financing selections. Arc’s enterprise debt resolution has phrases for as much as 4 years, maintaining charges near these supplied by banks, whereas their underwriting mannequin surveys threat effectively.

“Historically, it’s a really handbook offline labor-intensive course of, not only for the banks, but in addition for the operators of those very lean under-resourced startups, significantly on this funding setting,” he mentioned, explaining that with Arc’s digitally built-in strategy, funding will be determined in beneath 48 hours.

“We’re utilizing real-time information entry by means of back-end API integrations and a contemporary finance stack for our prospects to make on the spot algorithmically pushed underwriting selections,” Muir defined. “Our infrastructure, constructed in-house, permits us to seamlessly combine with the finance stacks of our prospects. And so in seconds, we are able to ingest thousands and thousands of historic monetary information factors.”

Whereas the method is digitally native, he defined that Arc additionally has a enterprise debt underwriting staff to examine the credit score selections earlier than signing off on the mortgage. The underwriting mannequin is then tweaked to enhance its course of.

Muir mentioned the choice to develop into Enterprise Debt comes as a direct response to the conversations Arc has with the founders they at the moment serve. Determined for a technique to develop, startups are in want of digitally-native, environment friendly financing options.

“It’s our responsibility to serve these firms, not simply on the banking facet, however on the enterprise mortgage sides as nicely. And we’re right here to satisfy that ask and work with our prospects to assist them develop and keep away from pointless dilution.”

{kind=link}