In a Nutshell

The article explores the transformative evolution of fee rails in finance, predicting a reshaped panorama with key traits similar to e-commerce surge, Open Banking adoption, and real-time fee shifts. It delves into unbundling monetary providers, the rise of revolutionary suppliers, and dynamic adjustments, analyzing the affect of open banking, real-time transfers, Tremendous Apps, massive techs, cryptocurrencies, and central financial institution digital currencies. The conclusion emphasizes the continued redefinition of fee infrastructure, stressing the necessity for banks to adapt and innovate for achievement on this dynamic surroundings.

Cost Rails Gaining Floor

Cost rails type the foundational infrastructure for safe and environment friendly fund transfers between people, companies, and monetary establishments globally, taking part in a significant function within the monetary ecosystem. In 2024, the monetary panorama will endure a transformative shift within the evolution of fee rails, reshaping the trade with vital implications for companies and shoppers. World digital fee transactions grew by 19% in 2021, exceeding pre-pandemic expectations. McKinsey tasks a 9% common annual progress within the international funds trade over the following 5 years, fueled by an e-commerce surge, Open Banking adoption, real-time fee traits, and the acceptance of ISO 20022 for enhanced information and standardization.

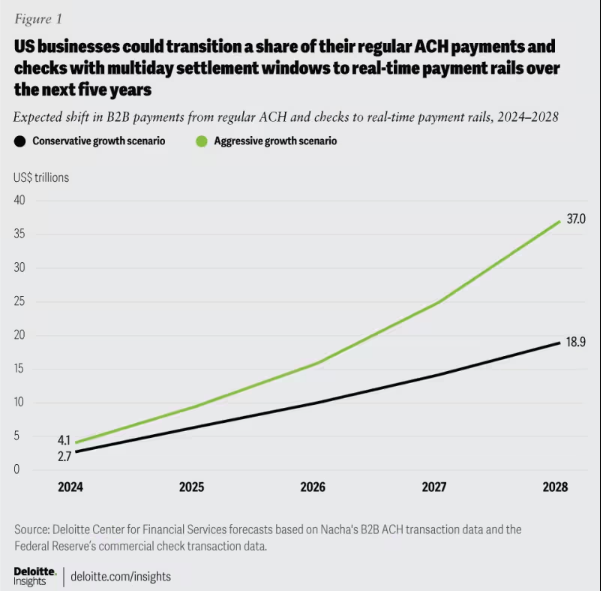

Determine 1: Anticipated B2B fee shift: Shifting from ACH and checks to real-time fee rails, 2024-2028.

As fee rails advance for pace, effectivity, and safety, staying knowledgeable is essential for banks. Adapting structure to evolving buyer wants is paramount, fostering resilience, adaptability, and long-term success in funds.

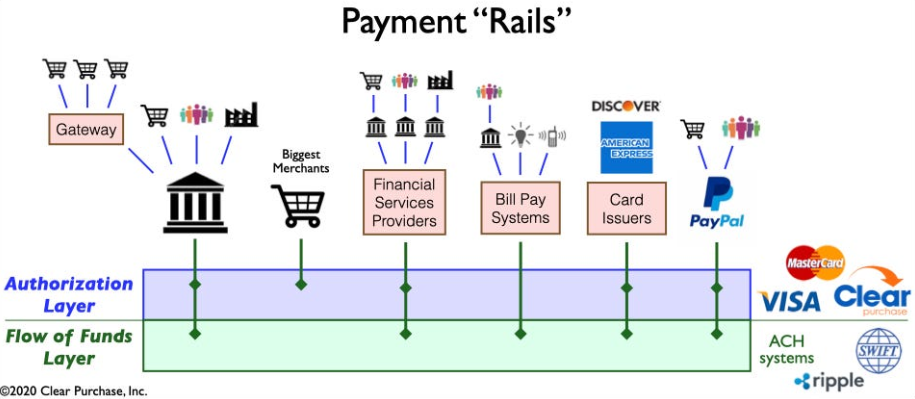

Determine 2: A Simplified View of Cost “Rails” Ecosystem

Unbundling of Monetary Providers: Taking Inventory of the Cost Panorama Transformation

The fee panorama transforms by the unbundling of monetary providers, pushed by fintech improvements like Venmo, Klarna, and PayPal. Whereas specializing in optimizing legacy processes, the phenomenon breaks down conventional bundled merchandise, permitting non-banks to focus on capabilities like fund holding and switch. This extends past B2C, reshaping the trade with new types of competitors and collaboration. Unbundling accelerates innovation, introducing real-time fee rails and integrating applied sciences like cryptocurrencies and open banking, resulting in a extra environment friendly and safe fee infrastructure.

Emergence of Revolutionary Cost Suppliers: In direction of Transmogrification of the Funds Panorama

A brand new era of revolutionary fee suppliers, like Sq., Adyen, and Stripe use cutting-edge know-how to simplify funds for retailers, capitalizing on the e-commerce increase. Disrupting the normal ecosystem, they provide environment friendly, safe, and cost-effective options, increasing fee strategies. The worldwide APM market is booming, with over 85% of enormous US retailers planning to simply accept new strategies, projecting a CAGR of 11.6% to achieve $27.8 billion by 2028.

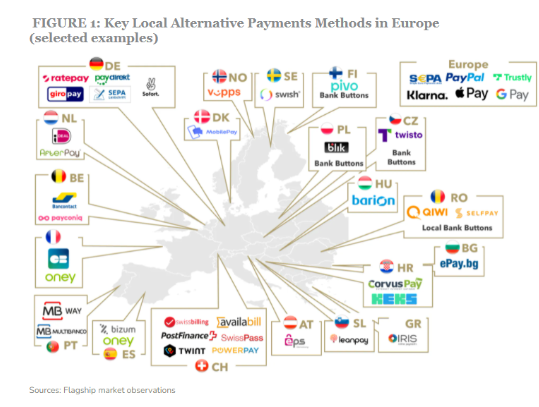

Determine 3: Some Key Gamers in Various Funds Technique Area in Europe

The ascent of those fee suppliers is additional propelled by the introduction of recent fee rails, similar to real-time fee rails and open banking. These developments facilitate quicker, extra environment friendly, and safer fee processing, permitting these suppliers to combine seamlessly into the fee ecosystem. This integration permits them to supply worth past funds, evolving into complete “one-stop retailers.”

Dynamic Shifts Influencing the Cost Panorama

A number of pivotal developments are intricately shaping the fee ecosystem, introducing complexity and fostering innovation:

Open Banking: This paradigm shift empowers smaller gamers to innovate in monetary providers by permitting third-party builders entry to monetary information, resulting in the creation of ingenious fee options and value-added providers.

Actual-time A2A Schemes: Profitable schemes like iDEAL, BLIK, and Pix allow immediate account-to-account transfers, driving innovation and competitors throughout the funds trade.

Tremendous Apps: Dominant in Asia, Tremendous Apps like Alipay and WeChat Pay supply a various vary of providers, together with funds, investments, and life-style providers, gaining reputation amongst shoppers and retailers alike.

BigTechs in Monetary Providers: Tech giants like Apple and Google are creating closed-loop monetary providers ecosystems round their pockets and fee capabilities, intensifying competitors and innovation.

Cryptocurrencies: Whereas not revolutionary in funds, cryptocurrencies persist and should affect the way forward for cash. Some banks discover their potential for fee options and cross-border transactions.

CBDCs: Central banks globally are growing Central Financial institution Digital Currencies (CBDCs) with the potential to exchange conventional fiat currencies, providing benefits like quicker transactions, decrease prices, and elevated monetary inclusion.

Intricate developments reshape funds, driving innovation and creating alternatives. Staying knowledgeable is essential for banks to remain aggressive within the evolving trade.

Revolutionizing Cost Infrastructure

The present wave of redefining fee infrastructure marks a departure from conventional fashions with two key evolutionary developments:

Development of New Cost Infrastructure: A shift in the direction of a next-generation setup, the place new and previous capabilities coexist in a multi-rail combine, is underway. Incumbent and challenger gamers compete for a redefined function within the worth chain.

Firms deploy new fee infrastructure, similar to PayPal’s Commerce Platform for multi-currency funds and Sq.’s all-in-one Terminal for varied fee strategies.

Exploration of New Cost Rails: Firms discover real-time fee rails and open banking. Mastercard’s Mastercard Ship and Visa’s Visa Direct allow real-time funds, driving blockchain innovation for cross-border and micropayments. AI and machine studying improve fee fraud detection.

The Backside Line

On the entire, the evolving fee rails are reshaping the way forward for monetary providers, fostering innovation and disruption. The battle round fee rails drives unprecedented adjustments amidst surreal solidarity and singularity of goal of key gamers within the fintech and monetary providers area, ushering in a brand new period within the funds panorama. Greasing the wheels to this dynamic surroundings will place banks and monetary establishments to search out their ft for monumental success.

{kind=link}