With compliance laws evolving recurrently and changing into extra demanding lately, banks and fintechs have needed to commit extra assets to maintaining with the shifting regulatory panorama and altering buyer expectations.

The stakes are excessive. Not solely do banks and fintechs face sizable fines and different regulatory punishments — equivalent to product shutdowns and jail sentences — for failing to stick to compliance guidelines, however they will additionally run afoul of their most necessary allies: customers. The looks of instability and untrustworthiness can shake the all-important relationship between banks/fintechs and their clients to their core.

For its 2023 State of Compliance Benchmark Report, Alloy – an organization that gives greater than 500 banks and fintechs an end-to-end identification threat answer and connects shoppers to greater than 190 sources of identification, fraud, and compliance information – surveyed greater than 200 professionals working in compliance-related roles at fintechs to be taught extra about their organizations’ compliance methods.

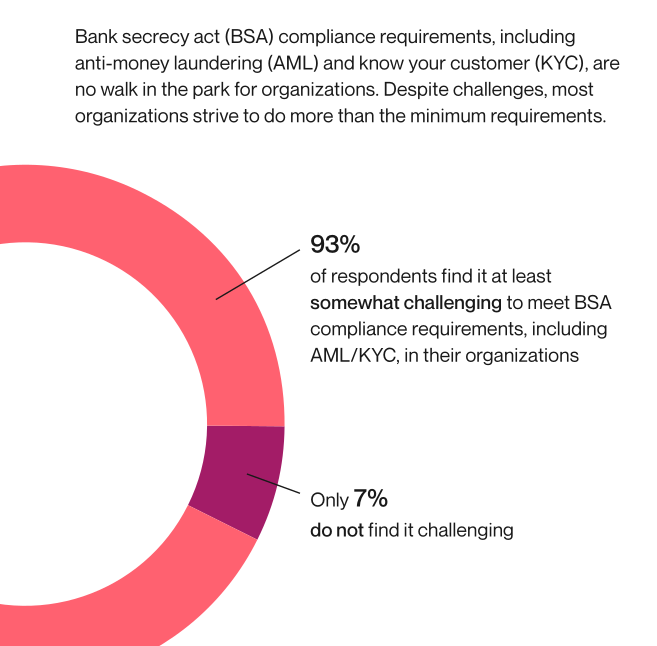

Alloy reported that 93 % of respondents discover assembly regulatory necessities no less than considerably difficult.

The identical report discovered that 55 % of these surveyed recognized an absence of automation as one of many greatest obstacles to assembly compliance necessities laid out by the Financial institution Secrecy Act. Unsurprisingly, 55 % are utilizing synthetic intelligence (AI)/machine studying to assist attain these targets. One other 29 % are exploring utilizing AI/machine studying for that goal.

Fintechs that use automated, data-backed programs to streamline compliance processes report having the ability to extra successfully fulfill regulatory necessities equivalent to Client Monetary Safety Bureau laws, anti-money laundering laws and sanctions issued by the Workplace of International Belongings Management.

Knowledge orchestration is an automatic course of that takes siloed information from a number of factors, organizes it and makes it usable for evaluation, serving to companies transfer to an automatic, holistic strategy, which is useful for:

- Complying with AML laws.

- Expediting the creation of suspicious exercise stories by making real-time information extra accessible.

- Serving to groups determine probably suspicious exercise by discovering how inconsistencies match collectively to type a bigger perspective.

For banks, compliance is changing into tougher as new steerage issued collectively in June by a trio of federal monetary businesses – the Federal Deposit Insurance coverage Company, the Federal Reserve Financial institution and the Workplace of the Comptroller of the Foreign money – offers them methods for managing their third-party relationships, together with these with fintechs.

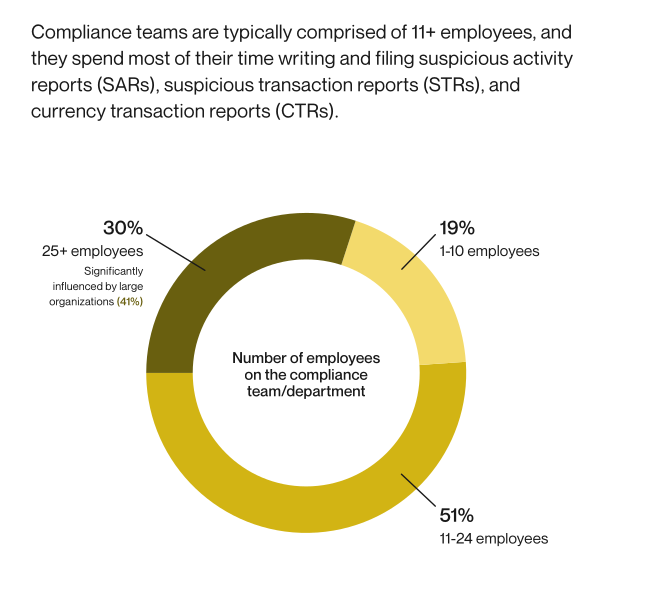

Alloy’s report exhibits that fintechs have began to speculate extra closely into assembly necessities set out by companion monetary companies in mild of the latest modifications to steerage. It reveals that 51 % of fintechs surveyed make use of compliance groups of 11-24 individuals, whereas 93 % categorical that they use no less than one third-party platform to help with compliance administration.

To discover how Alloy may also help organizations preserve tempo with regulatory compliance at onboarding and all through the shopper lifecycle, discover their compliance instruments and schedule an indication.

{kind=link}